While the recent budget deal in Congress took the debt ceiling off the table for the next two years (thankfully), one of the surprises of the deal was that it also sunset the ability to file and suspend social security. File and suspend was a tactic used by both individuals and couples and involved filing for one’s social security benefits and then suspending receipt of those benefits.

For couples, the strategy made sense if the following criteria were met:

- Both spouses were between full retirement age (typically 66 or a bit older)

- Neither spouse was drawing social security income

- They didn’t need the social security income

- Actuarially speaking, it was likely that both spouses would live a long life

When the above criteria were met, it made sense for the spouse with higher projected social security income to file for social security benefits and immediately suspend receipt of those benefits. That would then allow the spouse with lower projected benefits to file for spousal benefits, which are social security benefits calculated based on a spouse’s earnings record.

By following this strategy, the couple would receive some social security income while allowing both spouse’s primary benefit (i.e. the benefit based on their earnings records) to grow at roughly 8% per year through age 70. Assuming the couple was long-lived, the total additional social security income earned over their lifetimes could be several hundred thousand dollars. However, since file and suspend is no longer available after April 30, 2016, a spouse can only file for a restricted benefit if the other spouse has already filed for social security benefits – and that spouse can no longer suspend his or her filing.

An individual was also able to file and suspend his or her benefits at full retirement age. This was useful in those instances in which the individual did not need the social security benefit, but by filing and suspending, were something to happen to the individual (e.g. a terminal illness) the individual could claim the benefits foregone since filing and suspending as a lump sum.

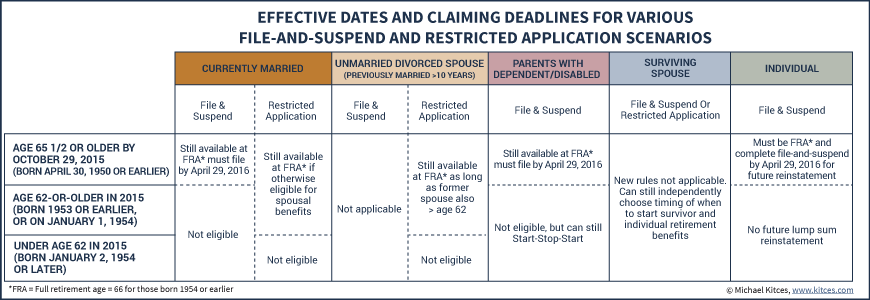

As I mentioned at the outset, the file and suspend strategy was sunset in the recent budget deal. The last date at which one can choose to file and suspend is April 30, 2016, although only those who were 65 ½ or older by October 30, 2015 and not already drawing social security benefits are eligible. This chart from Michael Kitces provides a useful overview of the deadlines and availability of both the file and suspend and restricted application strategies.

{kind=link}

We will introduce our new client portal when we release year end reports in mid-January. One of the first things you will notice with the new portal is the cleaner design. The portal also has a good bit of additional functionality, including:

- The ability to view information regarding your portfolio without generating a .pdf report. Instead, the information updates in real time within the browser.

- There are expanded options for information about your portfolio, including performance, holdings and account activity.

- If you have established a document repository with us to store estate documents and other information, we can now link directly to that repository from within the portal.

We will provide information on accessing the new portal when we launch in mid-January, but please feel free to contact us if you have any questions about accessing or using the portal.

![]()

![]()

As some of you may be aware, we’ve long used MoneyGuide Pro for our financial planning software. MoneyGuide recently launched a new service, MyMoneyGuide and we wanted to pass along information about the service in the event that you have colleagues, friends or family who may be interested in financial planning, but have yet to begin the planning process.

MyMoneyGuide is a 90 minute CFP® guided workshop in which users create a simple goal-based financial plan. While users are encouraged to have the plan reviewed by the planner who invited them to the workshop, they are under no obligation to do so and we cover the cost of the workshop.

More information about MyMoneyGuide, as well as a link to sign up for a workshop is available here.